A Letter to Jacob and Matthew about Early Career Personal Finance

Note – I was planning to write a private letter to my two sons Jacob and Matthew about early career personal finance. Because, well they are both just about in their early careers. I decided there’s nothing I would say in that letter that I don’t mind sharing publicly, so here it is. There are some revealing details about our financial history and current status. And this is a long letter.

TL;DR: Spend a lot less than you make to achieve financial independence and “retire” early.

Dear Jacob and Matthew,

You are both a few short months (Jacob) or just two years (Matthew) from your foray into the world of being financially responsible for yourself. I believe we’ve had a healthy, ongoing conversation about personal finance for over 10 years. You probably have the foundation of skills and experience to help you successfully navigate those early years. Still, I can’t help but add the classic “oh, just one more thing…” comment that parents are wont to do. Fair warning that this email will have more than just “one more thing.”

Let’s Do a Current Status Check

About 10 years ago I wrote about mini-retirement vs. semi-retirement. I’ve done quite a few things since that post, including:

- Being a founding CTO at a startup in Portland

- Taking another SVP of Engineering / CTO role at a mid-size company (WebMD)

- Become a writer and “coach of coaches” for Wing-T Youth Football

- Become a college instructor at WOU

- Become a trainer and coach helping technology professionals move up the leadership ladder

Since I left WebMD at the end of 2014, I’ve struggled with how to respond to the question “are you retired?” The answer to that has so many different implications to different people. That’s because so many people have a fixed mindset about what the trajectory of a career should look like. For most career-minded folks that go to college, the trajectory looks like this:

- Go to college and get a degree.

- Maybe that degree is enough for a fulfilling career. Maybe you also get a graduate degree (or two)

- Work for someone else and get a W–2 income

- Maybe go out on your own and freelance, or start a company once you are in a position to do so

- Do this until you are roughly in your 60s, then do what we call “retire”

I may have bought into this paradigm when I was in my 20s, but it wasn’t long into my 30s when I knew I wanted to find a different path. Tim Ferris first put words to what I had contemplated in the Four Hour Workweek which I first read in 2007. He used the word “mini retirement” as a mid-career break to travel, live abroad, or otherwise do lifestyle experimentation. You may remember that your mom and I did a mini retirement in 2007–2008, living at Keuka Lake with you as an experiment for most of the summer in 2008. I was able to put a lot more time into my two favorite hobbies at the time, photography and football coaching, plus spend time with you at summer camp here in NY. At that time we knew we had not met our long-term financial goals in any sense, but because of our lifestyle choices made throughout our marriage it was easy to take a significant break from what had been a $200,000+ annual income.

This also lead to a forward-thinking mindset that each time I have a career shift, or an opportune moment to quit and rethink the next step, I shouldn’t be afraid to experiment and try something totally different.

So back to that “are you retired?” question. The answer to that, for your mom and me, is “no”. But it probably isn’t the question people really mean to ask. To help get to the root of what they are likely asking (the question behind the question), I’m going to start answering:

I’m not retired, but Julie and I are financially independent. We are confident we can work as little or as much as we want and be secure through the end of our years.

What is this “financial independence” thing you speak of?

Recently I’ve been diving into different sources for personal finance (not Dave Ramsey this time), particularly blogs and podcasts focused on early retirement and financial independence (codeword is FI). Here are a few definitions to get us started:

Financial independence is the state of having sufficient personal wealth to live, without having to work actively for basic necessities. For financially independent people, their assets generate income and/or cash flow from dipping into the assets that is at least as great as their expenses. – Wikipedia

For me, financial independence is simple: it means that you are not beholden to a job to provide for your livelihood. Instead, your wealth – acquired through a high level of income or aggressive savings plan, supports your lifestyle. While you may still work, you don’t need to. You work because you enjoy it. – ThinkSaveRetire

Some common thinking about the math around FI is that if you can manage to save enough to have a net worth equal to 25 times your current living expenses, then you are financially independent. This comes from the Trinity study, which uses 4% withdrawal rate from your assets as a safe number that should allow you to preserve your net worth. Since the inverse of 4% is (1 / 0.04) = 25, accumulating a nest egg of 25 times your annual expenses is the threshold you would look for in order to have a very high probability that you won’t exhaust it. Therefore, if you have a net worth of 25x your current living expenses then you are financially independent.

For example:

- If you can live on $10,000 per year, you would need to save $250,000

- If need $100,000 per year to live on, you would need to save $2,500,000

(Notice how the target number changes dramatically depending on how much you spend each year? Hold that thought…)

There are some nuances to all of this math, such as if you have all of those assets tucked away into retirement accounts and want to start dipping into it in your 40s, you’ll likely pay penalties. Let’s not worry about details like that because there are two important variables we are working with here:

- What is your spending rate?

- What is your net worth?

Note that your income doesn’t have anything to do with this math, though during a time like now when mom and I are doing a wide range of different things (part-time work, independent consulting, selling digital products on line), that income effectively reduces “spending rate” number. This extra income can allow us to effectively live beyond our means. Like paying for an extra semester for Jacob, or planning a spring trip to Europe in 2018.

Physician on Fire fine tunes this math a bit more:

That’s how I’d like to define financial freedom. It’s your core spending + 2x(discretionary spending). For us, that’s annual spending of $40,000 + 2x($30,000) = $100,000 a year. If you could afford to spend double on those things you do to make life a little nicer, you’ve earned a newfound level of freedom. Financial Freedom.

Financial Freedom = 25 x (Core Spending + 2 x (Discretionary Spending))

– Physician on Fire

This equation is pretty helpful, especially when applied to the situation your mom and I are in because we’ve managed to shrink our core spending quite a bit, and then we make choices each year on discretionary spending based on a number of factors.

What do our numbers look like, and how did we get there?

There are two strategies your mom and I used to achieve financial independence.

- We grew our income over the years

- We grew our expenses at a dramatically lower rate than our income

A very influential book your mom and I read in the 90s, The Millionaire Next Door, talks about playing offense and playing defense when it comes to money. High income earners are playing great offense. Millionaires are characterized even more so by their defense:

Most of these households also play great defense; that is, they are frugal when it comes to spending for consumer goods and services.

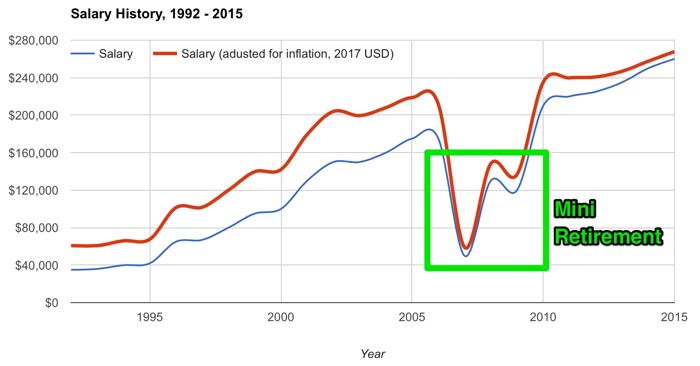

The figure above shows our approximate salary growth since 1992. This is close to reality (there were bonuses some years that might have adjusted things up or down by 15–20%), but does not include some significant windfall stock benefits from two of my employers.

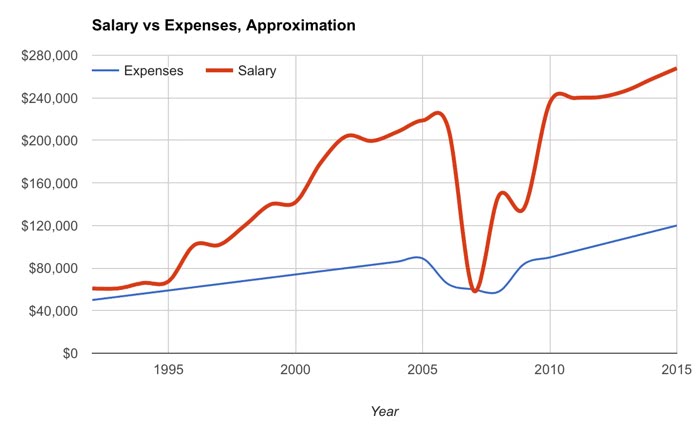

Even though we’ve been tracking expenses since first using Quicken back in the early 90s, I don’t have solid expense tracking aggregate data over those years. What I can report is that while we did grow our expenses, we grew them at a much lower rate than our income.

The chart above is an approximation of the changes in income and expenses over those ~25 years. This resulted in a net savings of about $2,000,000. When you subtract out some big ticket items that I wouldn’t include in a normal annual run rate (big trips like Galapagos or our Greek sailing trips, college tuition) I think this comes out about right.

So what do you think? Did we play good offense or defense? It is hard to deny that our offensive game was pretty strong. Still, there’s no way we would be hanging out at Keuka Lake each summer if we hadn’t played even better defense.

If you want to dive more deeply into the numbers behind this concept, Mr Money Mustache said it best:

The most important thing to note is that cutting your spending rate is much more powerful than increasing your income. The reason is that every permanent drop in your spending has a double effect:

it increases the amount of money you have left over to save each month

and it permanently decreases the amount you’ll need every month for the rest of your life

Read that, then read it again. Go read the whole article sons… I’ll be waiting for you here.

This concept is so freaking brilliant because it makes things so simple. You don’t have to pursue a great offensive game to achieve financial independence. If you always play great defense, the numbers work out automatically because your lifestyle will never expand beyond your income.

Calibrating how you got to where you are

While neither your mom nor I can claim to have come from poor households, we were both raised by frugal parents that valued the dollar. College was always in the cards for both of us as it was for you two. This fact alone puts you two into a very privileged class. Never forget the privilege that your genetic dice roll granted you. You’ve both worked extremely hard to achieve the success you’ve seen to date, but you had a huge lift by virtue of the following:

- Amazing public school system and teachers that had a big impact on your early years

- Parents who were able to take a very active role in your education as well as extracurriculars

- You were never lacking access to food, clothing, shelter, travel, and worldly experiences

- You have an extended family who have served as amazing role models for you as well as taken an extremely supportive interest in your well being

What should you be doing while still in college?

Be attuned to the things that bring happiness to you. Start paying attention to your relationship to money: when does it bring happiness, and when does it bring stress?

Your mom and I deliberately try to give you a lot of control over how you handle discretionary spending while giving a solid safety net during these years. We hope that you observe the duality of our generosity combined with, at times, extreme frugality. These two can be at odds at time. We tend to value spending money on experiences and family togetherness much more than we value spending money on things.

Your ability to live with essentially zero salary (or a pittance) at this stage is very important as you transition to your next stage.

It is OK to have credit cards at this stage (heck, you are into travel hacking just like mom and I are) but pay off the balances every month and use them as a tool for leverage.

Your first year after leaving college

This is mainly for Jacob right now; Matthew I’m sure I’ll amend this information in a few years.

Jacob, you are likely to graduate with attributes something like this:

- An income in the 6 figure range, depending on where you are geographically.

- About $30,000 in student loan debt.

In your first year, ditch that time bomb Subaru but buy a used car for about $5,000 that should serve you for several years. Find a housing situation that frees up as much cashflow as possible. Get into Dave Ramsey gazelle mode and pay off that student loan debt in the first year, while following the steps I outline below (meaning, you should absolutely contribute to employer-matched retirement savings first). Don’t rent furniture. In most cases, do the opposite of what many of your peers are doing with their new-found windfall income. Aspire to be the millionaire driving the 15 year old Subaru.

Note: This all changes if you get married right out of college. That requires another letter. Suffice it to say that it is important to find a mate that is financially and life-goal aligned with you.

Chris’ Toddler Steps

In closing, I want to offer my updated list of steps to help you towards financial independence. These are influenced by Dave Ramsey’s Baby Steps. I’m calling these toddler steps because I think if you start your career with a focus on financial independence you can break some of his rules.

You don’t move onto a subsequent step until you finished all of the steps before that.

- Build an emergency fund of at least $1,000

- If your employer has a matching contribution to a retirement plan, contribute enough to utilize this matching. This is essentially free money, a 100% return.

- Pay off all of your debt using the Debt Snowball, or your own modified sequence if it works for you. I trust you to make good choices here.

- Build 3 to 6 months of expenses in savings. This should be fairly liquid - many money market type funds will qualify here.

- Build in measurement systems and feedback loops to evaluate your spending as a percentage of your income. Be intentional about what you decide to spend money on, and be specially wary of anything that introduces new recurring expenses. Above all else, keep your spending rate as a percentage of income as low as you are comfortable doing. Funnel these savings into low cost broad market ETFs from Schwab or Vanguard.

The following are OK with the Chris Brooks toddler plan if you keep your wits about you:

- Credit cards when you are focused on maximizing rewards and have a bullet-proof system for managing them.

- Mortgages as long as you can avoid PMI.

Common traps that will screw you over while in step 5:

- Buying a new car. Your mom and I have done this many many times. We admit this was mostly stupid. At least we kept them on average for about 10 years and paid off every one of them within the first year. Instead, buy quality used cars (in the 4–5 year old range) for cash.

- Living in an expensive area. We chose Portland over Seattle because it looked like Portland would cost about 40% less than Seattle, and we were much more likely to see bad commutes in Seattle. Instead, consider some degree of geographic arbitrage.

- Growing expenses proportionally with your income because “you deserve it”. You are only hurting yourself here, just do the math. Let’s say you get a salary increase from $100,000 to $125,000. You decide not to change your lifestyle, therefore saving the extra $25,000. Let’s say that amounts to $18,000 after tax income. If you saved this and earned just 6% on it, in 10 years it would grow to about $250,000. In 20 years that would be almost $700,000. Instead, treat yourself to some special one-off benefit (like a vacation, or a special meal out, or a new video game console) but keep your lifestyle the same as it ever was.

- Layers upon layers of monthly services. I’m talking Verizon, Spectrum, Netflix, Hulu, Spotify, fitness clubs, beer of the month clubs, etc. These are easy to get into and you can get lulled into numb acceptance that it is normal. Instead, build in a periodic review process where you evaluate all of your periodic subscriptions and prune the shit you aren’t using or don’t value any more.

- Pursue the next McMansion, because that’s what your friends are doing. Bigger house with bigger yards just mean more expenses and more time spent taking care of it. Your mom and I joked about that when looking at some of the mansions in Ft. Lauderdale and the list prices - some in the “barely reachable” range for us. Our first mutual thought was “what about the operating expenses?” Exactly. The Keuka Cottages are expensive to keep and maintain, but we as an extended family have thrown our resources in together to make it doable and to keep it a special place for all of us. We kept our house in Sherwood, that we bought in 1998 for about $180,000, through all of those years of income growth because we couldn’t imagine how something bigger or nicer would make us any happier. Instead, be honest about the housing situation you truly need, and how a decision to upgrade might dramatically impact your long-term goals.

One final note on this “playing defense” mentality. This isn’t about deprivation, or saving everything until some later point in life when you can enjoy it. It is about thinking about where you want to be and making intentional choices about how to get there.

There are people achieving financial independence much earlier than mom and I did, who had significantly lower incomes. They focus on minimalism and extreme frugality, almost making a game of it. That approach is focused primarily on defense, and is a great strategy for people that choose professions without the same growth prospects as higher paying ones. That math will work either way, because these individuals become accustomed to a lower cost of living, their needs after achieving FI are also lower.

Love, Dad